How does it work when I want to withdraw my SIPP from Investengine? It says that IE does not support withdrawals, is this correct? If so, what’s the point of having a SIPP with IE? Am I missing something obvious? Thanks

1 Like

Good question. It was for this reason I left my pension with Vanguard, despite the higher fees.

Morning ![]()

![]()

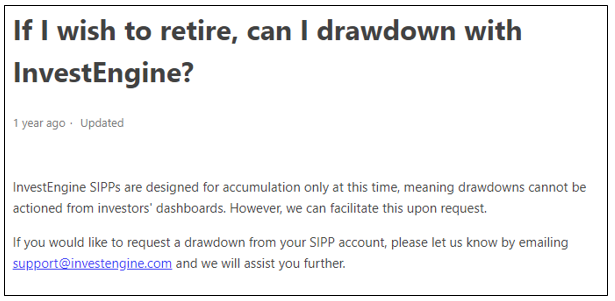

Have you seen this article?

2 Likes

If you will be saving into your SIPP for 20-30 years, they will probably have drawdown by the time you retire. If you are retiring this year, you will need to transfer out.

2 Likes

In May 2025 I was told by Client Services that “I can confirm we offer Flexi-Access Drawdown, as well as Uncrystallised Funds Pension Lump Sum (UFPLS).”

”The process involves filling of paper forms which we would prepare and send to you on request, and I can also confirm we do not charge for that service.”

1 Like

paper forms?? ![]() Hope that will change in the next 10 years or so otherwise I’ll probably just transfer to one that is all done online.

Hope that will change in the next 10 years or so otherwise I’ll probably just transfer to one that is all done online.

1 Like

My understanding is that the process is being done by another organisation who cannot use any of the information that IE currently holds about the owner.

As an update, the paper forms have to be printed, completed, scanned by the yourself and emailed back. Plus key documents have to be physically (in ink) certified by an official, such as a teacher. I have given-up and I am effectively doing what you suggested you would do when you retired.

3 Likes

Seriously? Omg what a pita and faff.

Bugger that. Will invest for some years and then transfer unless they improve their process

Thanks for the heads up

Got pensionbee and penfold Pension sipps that I can transfer to if needed

Hey maybe 212 trading get their act together and start offerings sipps

Unfortunately whilst T212 are excellent for ISA and GIA, they too have for years been promising a SIPP. In spite of the bad press I have found Freetrade SIPP to be excellent for trading in ETFs and stocks. The only issue is that like iE they are not really geared up for SIPP withdrawals and charge a high fee for each withdrawal.

My current plan for withdrawals is to do a partial transfer to a mainstream SIPP provider who will immediately do a UFPLS withdrawal. In spite of being upfront and honest with that SIPP provider they will do transfers-in for free and the withdrawals for free. So as long as I do not invest in any of their funds (which I will not because there will be no funds in that SIPP then the withdrawal process appears to be free of charge. I could not believe it but I was assured that is the case.

1 Like

I nearly transferred my SIPP to Fidelity then I decided against it. Now I just think that SIPPs are set up to transfer even more of money out of your pockets.

When I turn 57 (I am currently 51), I will liquidate any SIPP holdings I have with Invest Engine (only a couple of thousand thankfully) and and Fidelity (about 40k).

I will then dump the cash into my ISA (All World Fund).

Unless you’ve got a lot of money and are a higher tax payer, then I really think SIPPs are just tools to rob you.

If your total SIPPs are around £42k then it is difficult to argue against that. The only thing I would say is that by taking out the SIPP all at once (presumably with a UFPLS) then you will suffer Income Tax (admittedly at the Basic rate) on that withdrawal. You might consider withdrawing it in stages so that you avoid even basic rate Income Tax.

My plan is very complicated but where I avoid all Income Tax until around my 80s when my ISA savings finally run out and I have to withdraw meaningful amounts from my SIPP.

Obviously if tax allowances change between now and then I will adapt my plan.

1 Like

Yes, I would draw it all out in stages to avoid income tax. Fidelity do not charge for SIPP drawdown or withdrawals. If you use ETFs only then their platform fees are fixed at £7.50 a month which is very good. Invest Engine SIPPs seem to be nothing but complications.

1 Like

Isn’t Gandalf also called “Gandalf the Wise”? Your comments on SIPPs (“SIPPs are just tools to rob you”) don’t seem wise at all. Please get some advice before you do anything too radical.

2 Likes

i was thinking of transferring in 50k because of the low/no fees. But draw downs seem almost impossible to achieve, will a GP really sign my bank statement and passport for me. if i did transfer in i would need to then transfer out pre draw down, does anyone know or have experience of transferring out of IE?

Yes, I had exactly the same experience. Actually IE does a UFPLS (Uncrystallised Funds Pension Lump Sum) rather than a drawdown but insists on referring to it as a drawdown (which is something different).

I too met with this ridiculous signing procedure and rejected it.

By that point most of my pension was/is in a Freetrade SIPP but they charge £200+ for a UFPLS, so that option was also not feasible for me.

What I did was open a SIPP with HL, ask HL to transfer my IE SIPP to HL and then make a UFPLS withdrawal from them. [I have also transferred some of my Freetrade SIPP to HL and done a UFPLS withdrawal from HL.]

The HL side of the transfer was easy (you can even speak to a human to help you) and it is free of charge because they do not charge for withdrawals.

To be fair to IE, their side of the process was relatively easy in that all I had to do was print a form, sign it and upload it to IE.

I have now withdrawn all my personal funds from IE and I do not use them (other than remaining on this forum).

More recently Freetrade offers a SIPP free of charge, so (due to their wider range of shares and funds) their SIPP offer is better than offered by IE.

So my arrangement of paying into Freetrade and withdrawing the funds using HL works well. I believe most mainstream SIPP providers can be used for withdrawing funds in this manner.

[For complicated tax reasons I am paying into my SIPP at the same time as withdrawing from my SIPP.]

1 Like