One-sentence summary of the request:

Please consider implementing an alternative AutoInvest behaviour which would, instead of distributing available funds by the client’s target weights, invest the funds in order to nudge the whole portfolio towards the client’s target weights.

I’ll call this AutoInvest+Rebalance.

Below, I will give an example to explain the idea, and then provide some data to illustrate what kind of clients / portfolios would probably benefit from AutoInvest+Rebalance.

Let’s say I have a portfolio as follows:

| ETF | Weight |

|---|---|

| Equity A | 50% |

| Equity B | 50% |

On day 1, I put £1,000 into the portfolio and it is AutoInvested like so:

| ETF | Funds allocated | Unit price | Units bought |

|---|---|---|---|

| Equity A | £500 | £1.0 | 500 |

| Equity B | £500 | £2.0 | 250 |

A month later, equity A has had a good run and is now worth £1.25; equity B has stayed flat at £2. Now if I put another £1,000 into the portfolio, classic AutoInvest would do this:

| ETF | Funds allocated | Unit price | Units bought |

|---|---|---|---|

| Equity A | £500 | £1.25 | 400 |

| Equity B | £500 | £2.0 | 250 |

My resulting portfolio would now look like:

| ETF | Number of units | Unit price | Value | Weight |

|---|---|---|---|---|

| Equity A | 500+400=900 | £1.25 | £1,125 | 52.9% |

| Equity B | 250+250=500 | £2.0 | £1,000 | 47.1% |

… which is close to 50%/50%, but not quite. If I need to rebalance, I’ll have to wait a number of days for transactions to settle, hit the “rebalance portfolio” button, and incur some costs in bid-ask spread etc.

But AutoInvest+Rebalance would do the following:

- Work out the current value of the portfolio + the new funds;

| ETF | Unit price | Units held | Value |

|---|---|---|---|

| Equity A | £1.25 | 500 | £625 |

| Equity B | £2.0 | 250 | £500 |

| New funds | £1,000 | ||

| Total | £2,125 |

- Allocate the total value by the target weights, and work out the ETF units required to achieve this allocation:

| ETF | Weight | Target value | Unit price | Units needed |

|---|---|---|---|---|

| Equity A | 50% | £1,062.5 | £1.25 | 850 |

| Equity B | 50% | £1,062.5 | £2 | 531.25 |

- Buy ETF units in such a way to get to the target:

| ETF | Unit price | Units to buy | New funds allocated |

|---|---|---|---|

| Equity A | £1.25 | 850-500=350 | 437.5 |

| Equity B | £2 | 531.25-250=281.25 | 562.5 |

In one fell swoop, this operation would have bought just the right number of units of each ETF to achieve a rebalanced portfolio, skipping the wait and saving some costs on unnecessary transactions.

There will of course be cases where the portfolio has drifted too far away from the target weights, and/or the amount of new funds is not enough to achieve full rebalancing. In that case, we can either (1) make a best-effort attempt to get as close as possible to the target weight; (2) sell some ETFs if that’s what it takes to achieve full rebalancing; or (3) fall back on the classic AutoInvest behaviour.

Now for the data:

In the process of writing this post, I have wondered (as probably have you) if full rebalancing matters that much, when good ol’ AutoInvest already exerts partial rebalancing effect. I’ll try to answer that question using historical data:

Consider these 3 portfolios:

- Sane porfolio

- SSAC – MSCI All Country World Index 75%

- XGIU – Global inflation-lined bond 12.5%

- XG7S – Global government bond 12.5%

- Risky portfolio

- CXAP – Commodity ex-agriculture 59%

- EMIM – MSCI emerging markets IMI 38.5%

- HYGB – Emerging markets high yield bond 2.5%

- Heart attack portfolio

- XMBR† – MSCI Brazil 13.5%

- GJGB – Junior gold miners equity 40%

- SPDM – Physical palladium 46.5%

† InvestEngine does not have XMBR, but I need an MSCI Brazil ETF that is accumulating and has a sufficiently long history.

And consider the following scenarios:

- Monthly AutoInvest of fixed amount, with vs. without rebalancing

- Quarterly AutoInvest of fixed amount, with vs. without rebalancing

- Semiannual AutoInvest of fixed amount, with vs. without rebalancing

- Yearly AutoInvest of fixed amount, with vs. without rebalancing

Using end-of-month price from Nov 2018 to Nov 2022 (that’s the longest whole-year period common to all the ETFs I used), I simulated the 4 scenarios using the 3 portfolios, calculated the percentage difference in portfolio value with vs. without rebalancing, and plotted the following graphs:

Sane portfolio:

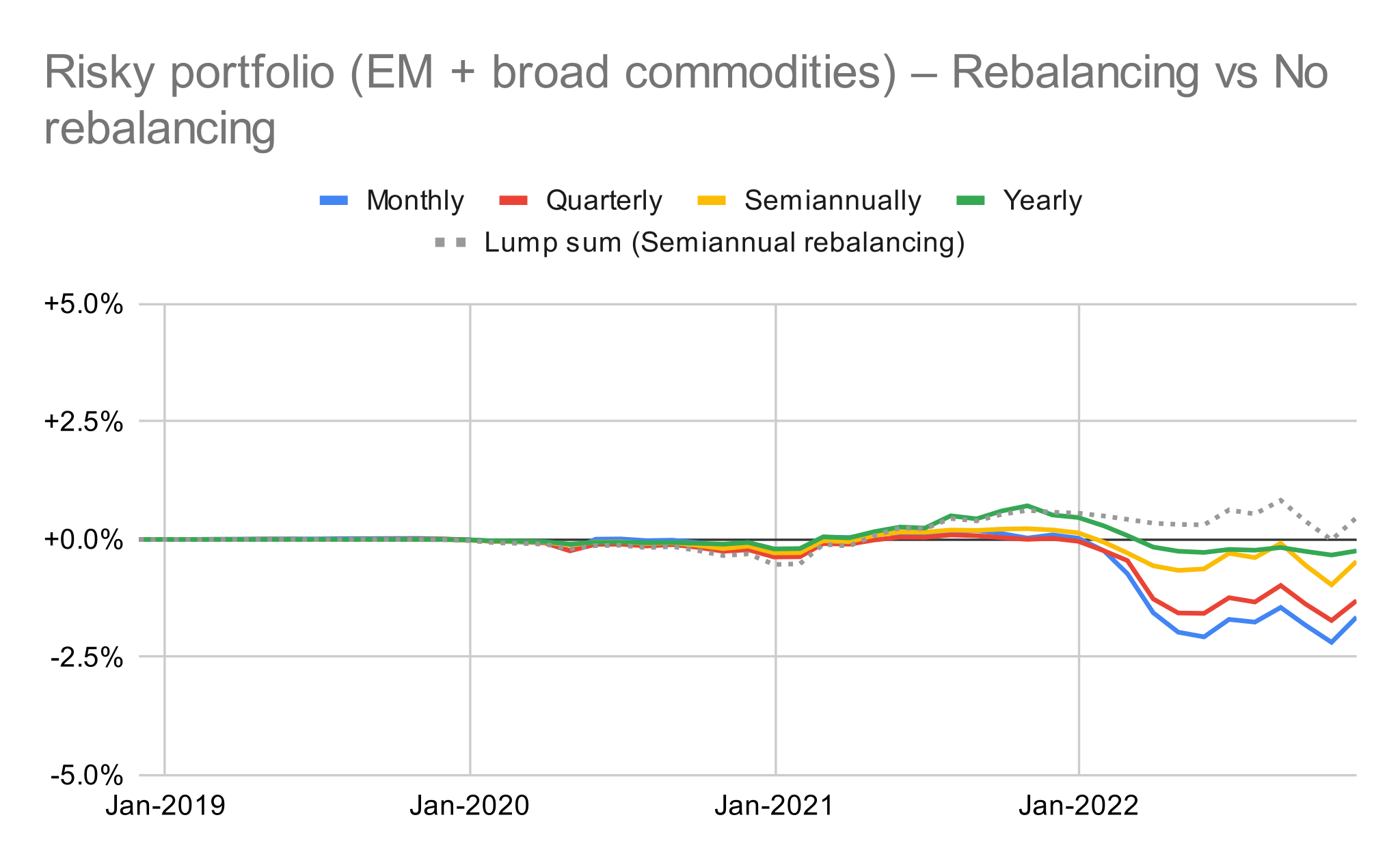

Risky portfolio:

Heart attack portfolio:

The charts depict the relative performance with vs. without rebalancing. A positive value means rebalancing outperforms no rebalancing.

From these charts we see:

- For the sane portfolio, the difference with vs. without rebalancing is not prominent, just within ±0.5%.

- For the risky portfolio, the difference starts to show after Jan 2022. Rebalancing underperforms as commodities continue their year-long climb but rebalancing causes funds to flow out of CXAP and into the less profitable EMIM and HYGB. In any case the effect is still muted, within ±2.5%.

- For the heart attack portfolio, the real make-or-break moment happened between Feb and Apr 2020. In Feb 2020, a huge spike in SPDM price means rebalancing (which occurred for the monthly and quarterly scenarios, but not the semiannual and yearly ones) causes funds to flow out of SPDM and into XMBR and GJGB. The subsequent steep drop in SPDM hurts the non-rebalanced portfolio much more than the rebalanced one. After Feb–Apr 2020, the monthly and quarterly scenarios retained the performance differentials between the rebalanced and non-rebalanced portfolios, with the rebalanced portfolio outperforming by >5% by the end of Nov 2022. The semiannual and yearly scenarios did not experience this shock and carried on to evolve gradually, both ending up with rebalanced portfolios outperforming by around a modest 1.5%.

From these simulations we can observe:

- Rebalancing has more prominent effects when done monthly and quarterly than semiannually and yearly.

- Rebalancing also has more prominent effects when done on portfolios with more volatile ETFs.

- This probably does not mean rebalancing more often is always better. Whether rebalancing wins or loses really depends on the how the ETF prices move around the time of rebalancing. (In our “heart attack portfolio” above, rebalancing has helped reduce exposure to an ETF that experienced a huge upward spike and then subsequently performed poorly.)

- Huge gains or losses in rebalancing vs. no rebalancing tend to stick around, because these unusual price movements that make or break the strategy don’t happen often.

In conclusion:

AutoInvest+Rebalance may benefit clients who (1) hold volatile ETFs; (2) invest regular amounts every month or quarter; and (3) have the conviction that their preset ETF weights should be strictly adhered to. For these clients, having the AutoInvest+Rebalance feature can save time and costs, compared to classic AutoInvesting + wait until transactions settle + press “Rebalance portfolio” button.